Table of Contents

Introduction

Summary: Mobile home taxes in 2026 are governed by a binary classification system: Real Property (taxed like a house) or Personal Property (taxed like a vehicle). This guide explores how land ownership, foundation engineering, and state title laws dictate your annual tax bill. Failing to understand your home’s classification can lead to seizure of property for unpaid back taxes or the loss of thousands in IRS capital gains exclusions. This is the definitive technical breakdown for homeowners and investors aiming to maximize Net Worth Trajectories over a 10-year hold.

Note: Local labor rates for foundation retrofitting and title retirement change constantly. See our full regional cost table below.

Video Guide Overview

Affiliate Disclosure: This post contains links to tools and services that help manage property taxes. We may earn a commission at no cost to you.

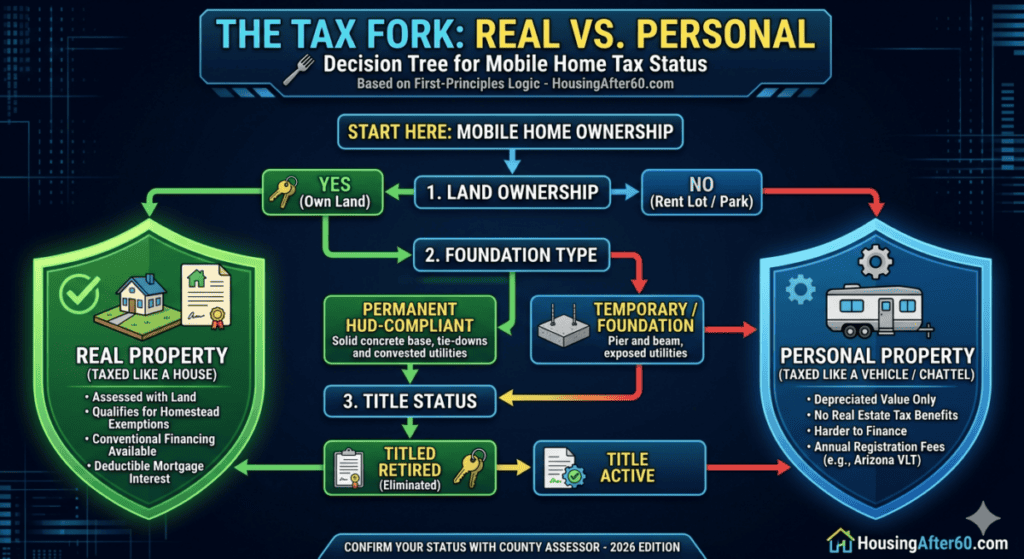

The Short Answer: The Binary Nature of Manufactured Housing

In 2026, the tax man views a mobile home as a “chameleon.” If it sits on wheels in a park where you pay lot rent, it is Personal Property (Chattel). You pay a fee similar to a car registration. If you bolt it to a permanent foundation on land you own and legally “retire” the title, it becomes Real Property. This distinction is the single most important factor in your Total Cost of Ownership (TCO). Most rookies look at the monthly payment; pros look at the Tax Classification. If you don’t know your status, you don’t know your ROI.

The Two Ways Mobile Homes Are Taxed

1. Real Property (Real Estate Tax)

When a home is classified as Real Property, it is lumped in with the land value. The county assessor views the home as an “improvement” to the real estate, much like a stick-built house. Requirements typically include owning the land, having a HUD-compliant foundation, and completing a Title Elimination process. You pay this annually or semi-annually through the County Treasurer. This classification allows for Appreciation and access to 30-Year Fixed Financing.

2. Personal Property (Chattel/Vehicle Tax)

If you rent a lot in a Mobile Home Park, you are likely paying Personal Property Tax. In states like Arizona, this is called a Vehicle License Tax (VLT). It is often cheaper annually but offers zero appreciation benefit and creates a “wasting asset” scenario. In 2026, many parks are passing their own land tax increases directly to tenants through “tax pass-through” clauses in leases, meaning you pay the home tax and a portion of the park’s real estate tax.

2026 Cost Transparency Table: Category Comparison

| Category | DIY / Basic (Park) | Pro / Premium (Owned Land) |

|---|---|---|

| Annual Tax Rate | $150 – $600 | $1,200 – $3,500 |

| Valuation Method | Depreciated Book Value | Market Appraisal |

| Homestead Discount | $0 | $250 – $1,500 (avg) |

Technical Deep Dive: IRC Section 121 and the $250k Exclusion

One of the biggest mistakes mobile home owners make is assuming they qualify for the Section 121 Capital Gains Exclusion. This allows you to exclude up to $250,000 (single) or $500,000 (married) of gain from the sale of your primary residence. However, if your home is classified as Personal Property, the IRS rules become murky. To safely trigger this exclusion, the home must be your principal residence for two of the last five years. If you sell a mobile home in a park, the IRS may treat the “gain” as the sale of an asset, not a home. As an investor with 100+ flips, I always advise owners to verify their 1099-S reporting status before listing. If the home isn’t Real Property, you might be handing the government a check for 15-20% of your profit in Capital Gains Tax. This is why Land Ownership is the ultimate tax shield.

What Determines Your Tax Status?

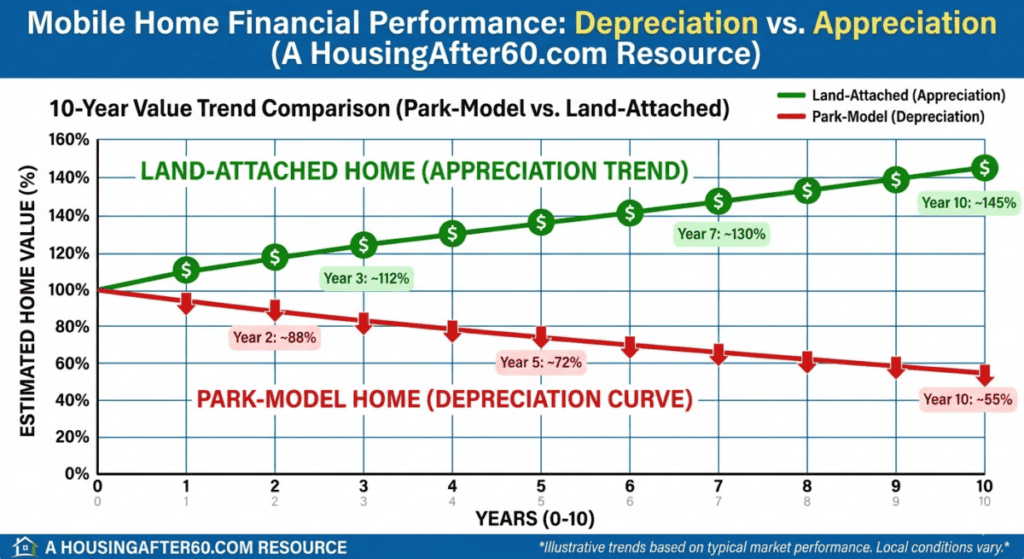

Land Ownership & Subsurface Utility Engineering (SUE)

Owning the land is the first step, but it is not the last. To the tax assessor, a home is only “permanent” if its connection to the earth is total. This includes the quality of your water, sewer, and electrical tie-ins. In 2026, many jurisdictions are requiring SUE Quality Level A (precise mapping via vacuum excavation) before a title can be retired on a land-home package. If your utilities are “temporary” (e.g., exposed PVC or heat-taped lines), the county may categorize the home as Personal Property regardless of your foundation. This is a $10,000 mistake. A home classified as personal property due to utility non-compliance depreciates at 3-5% annually, whereas the same home with SUE-certified underground utilities can appreciate along with the land.

Permanent Foundation Systems & HUD Compliance

A “permanent” foundation isn’t just concrete blocks. In 2026, many lenders and tax assessors require a HUD-compliant foundation with tie-downs that meet specific Seismic or Wind Zone requirements. If the wheels, axles, and hitch are removed, the home is one step closer to Real Property status. For more on this, read: Exploring The Resale Value of Mobile Homes

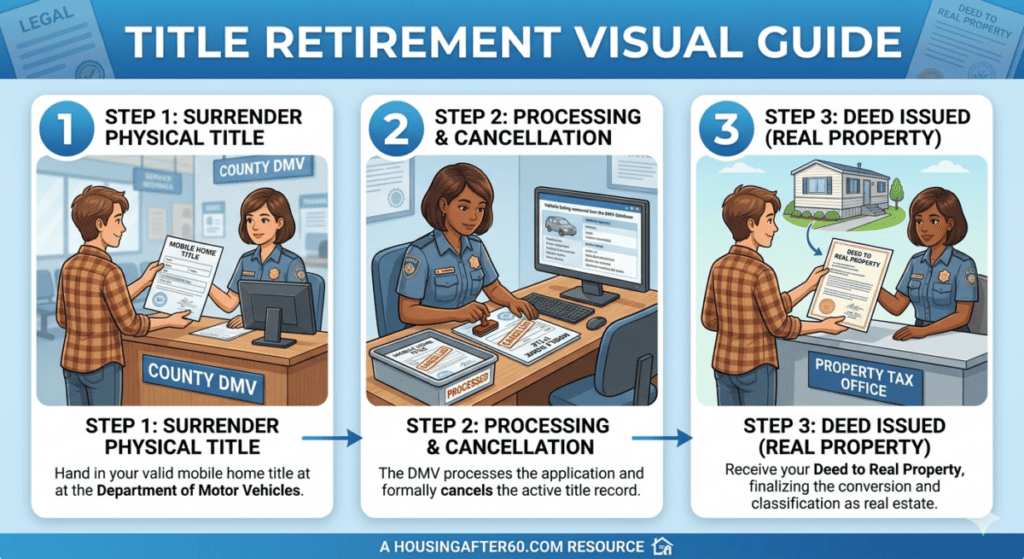

Title Status & The Elimination Process

Every mobile home starts with a Title (like a truck). To stop paying vehicle-style taxes, you must undergo Title Elimination. This is a legal process where you surrender the title to the state and record an Affidavit of Affixture. Once recorded, the home and land are “married” for tax purposes. If the title is “active,” you are paying Personal Property Tax, which means you are missing out on Mortgage Interest Deductions.

2026 Cost Transparency Table: Real Property Conversion

| Category | DIY / Basic | Pro / Premium |

|---|---|---|

| Foundation Retrofit | $1,800 – $3,500 | $5,500 – $9,000 |

| Engineering Certification | N/A | $450 – $750 |

| Title Legal Fees | $150 | $800 – $1,200 |

Technical Deep Dive: Zoning Variance Logic

Before you even think about taxes, you have to deal with Zoning. If you buy a mobile home and try to place it on a lot, the Zoning Board may deny your Real Property conversion based on the Year of Manufacture. Many municipalities in 2026 have banned homes built before the 1976 HUD Code. If your home is older than 1976, it is almost impossible to classify it as Real Property. You will be stuck paying Personal Property Tax on a home that is technically “illegal” to move or install. Always check the HUD Tag (the red metal plate) before you sign a contract. If the tag is missing, you may be forced to pay for a HUD Certification Label, which can cost $1,000+ and delay your tax reassessment for months.

The 10-Year ROI Net Worth Trajectory

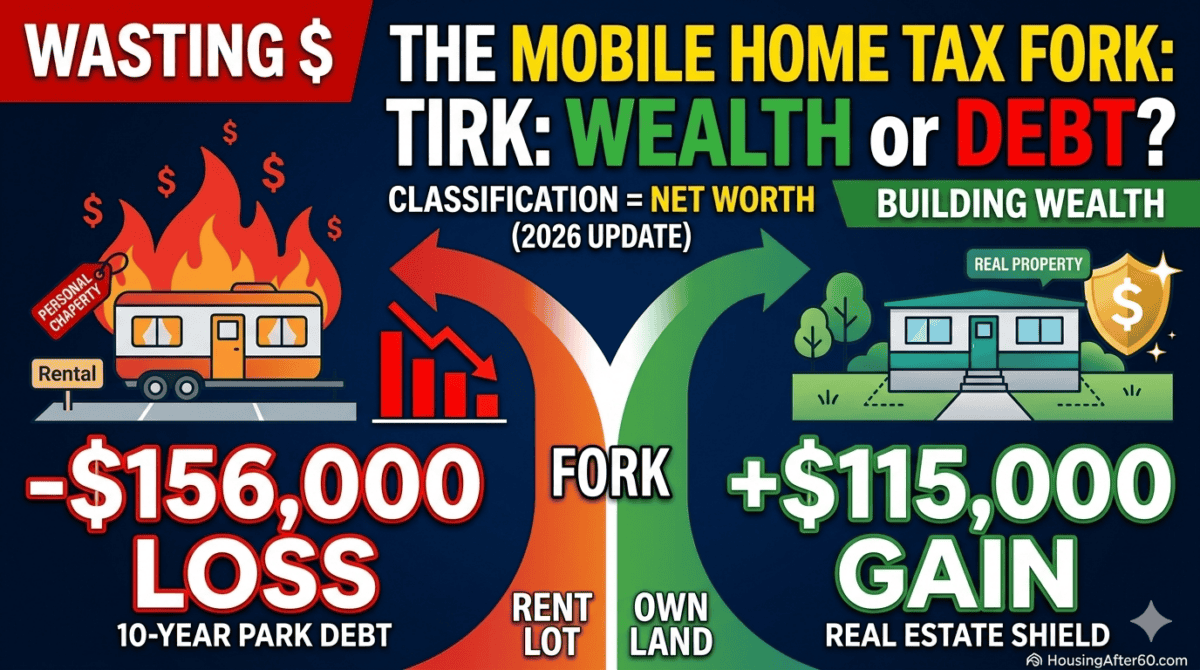

Let’s look at the First-Principles Logic of net worth. If you buy a double-wide in 2026 for $150,000, your tax classification determines your 10-year financial health.

Scenario 1: Personal Property (Park Model)

Your taxes are low (approx $300/year), but you are paying $800/month in lot rent. Over 10 years, you’ve paid $96,000 in rent (non-deductible) and your home is now worth $90,000 due to depreciation. Your net position is a loss of $156,000.

Scenario 2: Real Property (Land-Home Package)

Your taxes are 300% higher (approx $2,000/year), but you own the land. Over 10 years, you’ve built $50,000 in equity. The land has appreciated by 3% annually, and because the home is “Real Property,” it has appreciated with it. Your 10-year net worth gain is approximately $115,000.

The “tax savings” of a mobile home park are a mathematical illusion. High-tax Real Property is almost always the superior wealth-building vehicle because it allows for capitalized asset growth rather than expense-heavy consumption.

Buying or Selling — The Tax Landmines

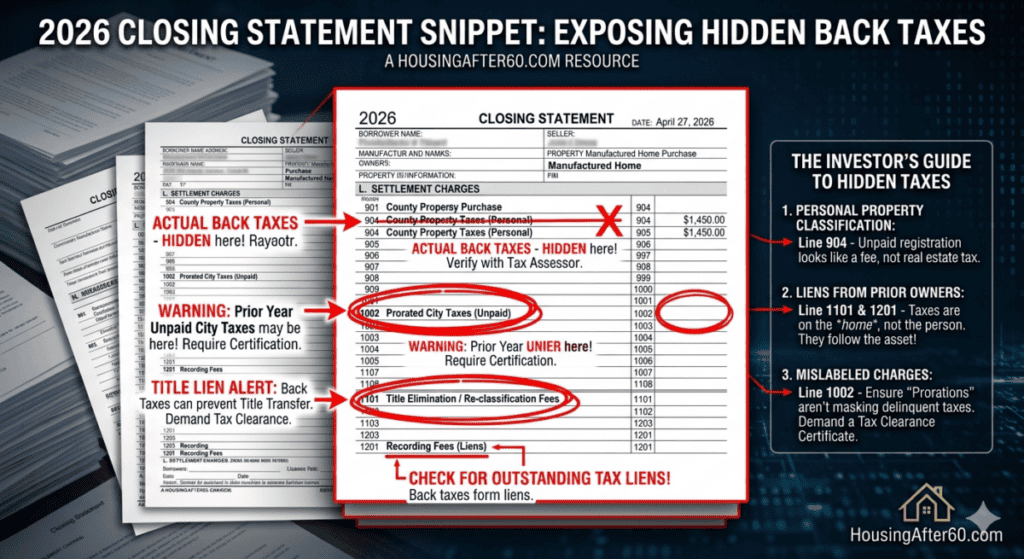

The “Back Tax” Trap

In 23 years of flipping, I’ve seen more deals die because of unpaid taxes than bad roofs. In many states, Personal Property Taxes follow the home, not the owner. If you buy a home with 5 years of unpaid registration fees, YOU are responsible for them the moment you transfer the title. Always demand a Tax Clearance Certificate before closing. For a full breakdown, see: Mobile Home Financing Options Explained.

Investor Logic for MHP Portfolios

For the pro investor, Ad Valorem taxes are the enemy of Cap Rate. When managing a portfolio of units, the difference between Personal Property and Real Estate taxes changes your Net Operating Income (NOI) calculations. In 2026, Real Property homes are easier to bundle into commercial securities. By investing in Title Elimination, you can re-classify a portfolio as Real Estate. This move typically increases the Exit Multiple by 2.5x. You are essentially paying a small “tax tax” to unlock a massive liquidity premium.

Affiliate Comparison Table: Inventory & Tax Management

| Tool Name | Primary Use | 2026 Pricing |

|---|---|---|

| PropTaxSlayer | Automated Tax Bill Appeals | $49/year |

| TitleVerify Pro | DMV Title History & Liens | $19 per Search |

Actionable Checklist: Avoid 2026 Tax Liens

- Check the HUD Plate: If the red metal plate is missing, you cannot convert to Real Property easily.

- Audit the Title: Ensure no Department of Revenue liens exist. These don’t always show on a standard real estate search.

- Call the County Assessor: Confirm the Parcel Number matches the home’s VIN.

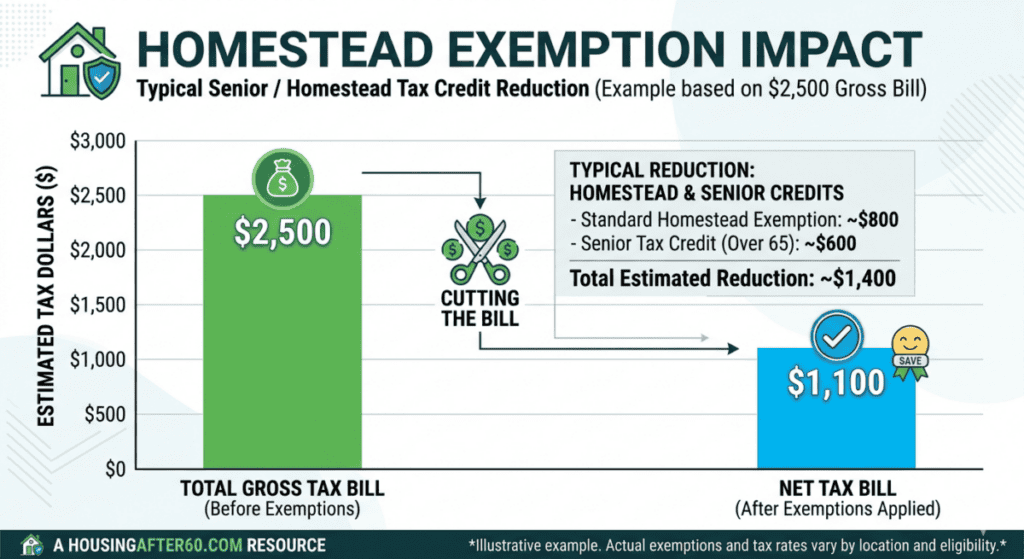

- Apply for Homestead: If you own the land, do this immediately to save up to 30% on your bill.

- Review SUE Compliance: Ensure utilities are below the frost line and metered correctly for Real Property status.

- Verify the 2026 Mill Rate: Many counties have updated rates; don’t rely on 2025 numbers.

2026 Regional Cost Table: National Trends

| Region | Avg. Property Tax (Real) | Avg. Registration (Personal) | 2026 Trend |

|---|---|---|---|

| Southeast | $1,850 | $220 | Increasing (Insurance-led) |

| Southwest | $2,100 | $195 | Stable |

| Midwest | $1,350 | $95 | Decreasing (Incentives) |

| West Coast | $4,800 | $600 | Aggressive Growth |

Final Thoughts from Charles O’Dell

The government doesn’t care about your “dream home”—they care about the Tax Classification. If you want to build wealth in manufactured housing, move the home toward Real Property status as fast as possible. It stabilizes your taxes, secures your financing, and protects your IRS exclusions. If you stay in the Personal Property lane, you are essentially driving a house that the tax man treats like a 1998 Honda Civic. Choose wisely. For more on mobile home investment strategy, visit Are Mobile Homes A Good Rental Investment?

About the Author: Charles O’Dell

Charles O’Dell is the founder of HousingAfter60.com. With over 23 years in the industry and 100+ successful mobile home flips, Charles has seen every tax mistake in the book. He specializes in Title Elimination, Foundation Retrofitting, and Investor ROI Trajectories. He doesn’t believe in “fluff”—he believes in First-Principles Logic and Technical Accuracy.

Written by Charles O’Dell, a 23-year real estate veteran with 100+ mobile home flips.