Table of Contents

Introduction

Updated for 2026+: This article reflects current manufactured housing rental realities, including post-2024 financing conditions, park ownership trends, insurance availability, and state-level title and tenancy variations. Data points and guidance are intended to remain relevant through 2026 and beyond, with emphasis on long-term risks, compliance factors, and investor due diligence.

Investors are always looking for a solid place to invest their money that provides safety (preservation of capital) and a great return on their investment (ROI). As I poke around on the internet I find too many blurbs about how mobile homes only depreciate and are a bad investment. Our experience has been much different.

Disclosure: Some links below may be Amazon affiliate links. As an Amazon Associate, MobileHomeFriend.com may earn a commission from qualifying purchases. This does not affect price or content neutrality.

Video Guide Overview

Short Answer

Short Answer: Mobile homes can be a viable rental investment in specific situations, particularly when acquisition costs are low and operational risks are well understood. However, outcomes vary significantly based on whether the home is located in a park or on owned land, how title and insurance are handled, and how local regulations affect tenancy and resale. This is not a uniform or passive investment class.

- Mobile Homes Can Appreciate – Much like a stick-built home. The understanding of appreciation rather than depreciation is important. The mobile home appreciation rate may be slightly less, but they certainly do go up in value if purchased properly.

- Mobile Homes Rentals Offer A High Rate Of Return (ROI) – A good return on investment is the pillar rule for wise investing. Most real estate investments require a highly leveraged mortgage position and a good appreciation rate in order to provide a solid ROI. Mobile homes can offer a great return without any leverage or appreciation.

- Mobile Homes Are Inexpensive To Renovate – In our experience, we are able to completely renovate a mobile home for investment at a fraction of what it costs to do a traditional home.

- Mobile Homes Are Inexpensive To Maintain – The systems in a mobile home (plumbing, HVAC, electrical) have much easier access than in a stick-built home. Mobile homes tend to be smaller than most stick-built homes. We find it costs us far less to maintain a mobile home over the long haul than a traditional property.

- Mobile Homes Have A Large Market Interested In Renting Them – There is a far larger population of average to less than average income earners in most areas. We have always found it extremely easy to rent out our mobile homes to quality tenants.

- Mobile Home Tenants Tend To Stay Longer Than In Traditional Homes – In our experience, we have been able to keep tenants in our properties for many years. This is far longer than the typical six months to 1 years turnover rates on traditional homes.

Risks, Pitfalls, and Common Misunderstandings

One of the most common misunderstandings is assuming that mobile home rentals behave like traditional single-family rentals. In practice, depreciation, tenant turnover, and resale liquidity can differ substantially. Investors often underestimate park rule enforcement, lot rent escalation, and the difficulty of financing or insuring older homes. Another frequent error is assuming that low purchase price alone ensures strong cash flow without accounting for maintenance intensity, vacancy risk, or regulatory constraints.

State-by-State and Real-World Variation

Rental outcomes vary widely by state. Some states treat manufactured homes as personal property by default, affecting taxation, eviction procedures, and lien rights. Others allow conversion to real property under specific conditions. Park-owned versus resident-owned communities also change risk exposure. Investors should confirm whether local jurisdictions impose rent control, tenant protections, or park closure notice requirements that materially affect exit strategies.

Practical Investor Verification Guidance

Before purchasing a mobile home for rental use, investors should verify title status, age of the home, park acceptance policies (if applicable), insurance availability, and local eviction procedures. Confirm whether the home can be legally rented, whether park management must approve tenants, and how lot rent increases are structured. Written confirmation from park management and local authorities is preferable to verbal assurances.

Understanding whether a manufactured home is titled as personal property or real property is critical for rental investors. Title classification affects financing, taxation, insurance, and resale options. For a detailed explanation of how these classifications differ, see this breakdown of mobile, manufactured, and modular home definitions.

Mobile Homes Can Appreciate

A commonly held belief is that mobile homes only depreciate. Let’s explore why that is the case. Just like with a car, which depreciates up to 10% the second you drive it off the lot, a brand-new mobile home will also drop in absolute value.

I say absolute value, because when a new mobile home is purchased there are farm more costs associated with it than just the cost of the mobile home. For example:

Additional Costs Over Just The Cost Of The Home For A New Mobile Home:

- Permits and moving fees

- Cost to transport the home from the dealer to the mobile home lot

- Cost to prepare the lot for setting up the mobile home

- Cost to actually set up the mobile home on the lot

- Utility connection costs

- Cost to skirt the mobile home

- Cost for any porches and awnings

- Cost for HVAC compressor and condenser unit

These costs can be VERY expensive. Running from minimum of about $10,000 up to $40,000 or more. Remember, these costs are over and above the original purchase price paid for the actual new manufactured home.

After completing the setup of the home and the lot, if you immediately put the new mobile home up for sale, you may not be able to recoup all of your investment.

But, most manufactured homes that are sold are not purchased as new. They are existing homes that are already set up in either a mobile home park or on their own land. These, like any other dwelling, can be in impeccable condition, or in absolutely terrible condition, and the price you pay should reflect that.

EXAMPLE

Last year we purchased this 1998 doublewide:

- On its own land (6,000sf lot) in a manufactured home subdivision

- 2,200sf of living space with 4 bedrooms and 2 bathrooms

- Vacant for over 8 years

- Home was in very poor cosmetic condition

- Missing HVAC system

- Missing water heater

- Missing all flooring

- Missing skirting

- Broken windows

- Rotted front porch

- Many holes in subfloor

At the time, like homes in the area that were in good condition were being sold for around $150,000. Because of the condition of the home, we were able to make the purchase for $52,000 all in.

We had calculated, prior to making the purchase, that it would cost us around $40,000 to bring the home up to our standards. We went over our budget by about $6,000 in renovations. When we were finished, our all-in investment in the home was $98,000.

This home was rentable in the area for $1,450 per month or $17,400 per year. That is a gross cash on cash annual return on investment of 17.75%. That return was possible without any leverage through a mortgage, or any annual appreciation on the home.

With this particular home, we ended up selling it for $164,000 for a profit of $66,000. That was a 67% return on investment (ROI).

Also, as long as that home is maintained in good condition, its value will move up and down with the market like any other property. Our market here in Mesa, Arizona has gone up in value about 6% from 2017 to 2018. That home has appreciated and is now worth over $175,000.

The purpose of this example is to show that manufactured homes can indeed appreciate in value like other properties. It all depends on how you make the purchase.

We routinely purchase homes in mobile home parks, and on their land. By making sure we purchase correctly, we’ve been able to make similar returns on each mobile home we’ve invested in.

Mobile Home Rentals Offer A High Rate Of Return (ROI)

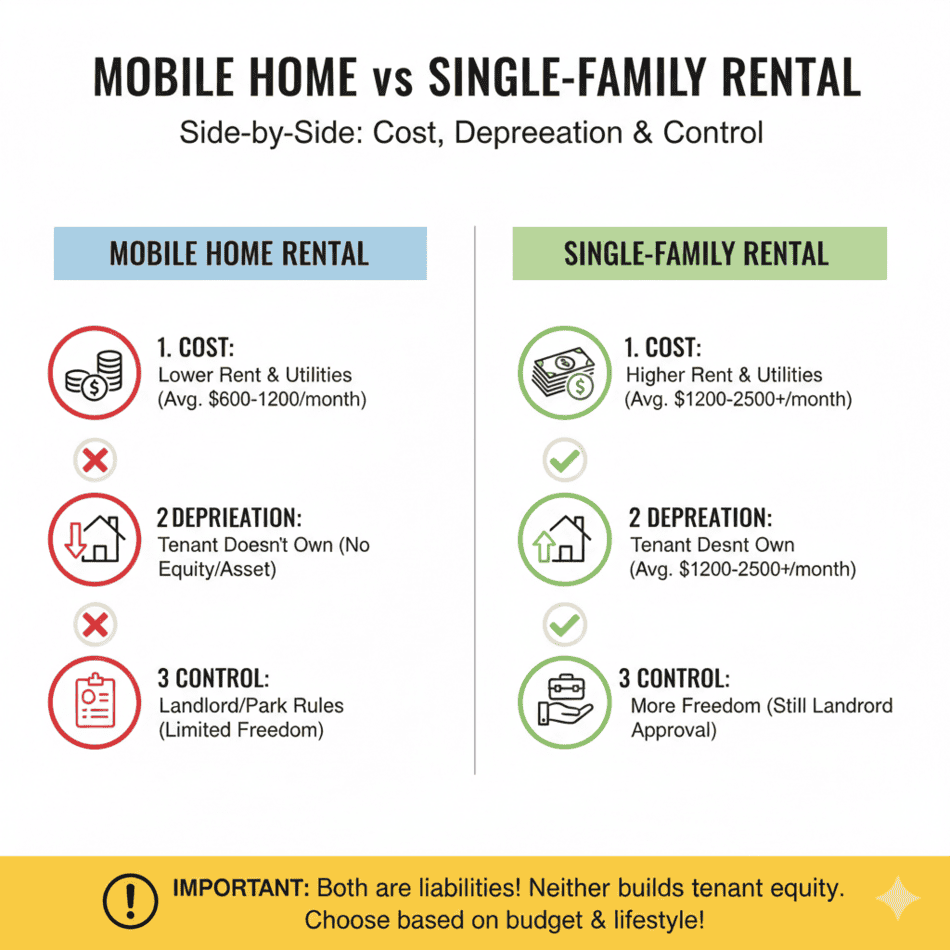

Let’s compare the rate of return you might get off of a traditional site-built rental home vs. a mobile home in a park or a mobile home on its own land. Mobile Home Friend operates in the Phoenix, Arizona market, so the figures we will show you have to do with the returns we get from our market.

For expenses we will assume the following:

- $1,500 annual property taxes for site-built home

- $850 annual property taxes for mobile home on its own land

- $175 annual taxes for mobile home in a park

- $750 annual insurance for site-built home and mobile home on its own land

- $400 insurance for mobile home in a park

We will be assuming that cash is paid for any of the properties as is often done in our market. Running calculations in your market will be similar once you have done some research to gather the pricing and rental information.

TRADITIONAL SITE-BUILT HOME

A typical 1,400sf, 3 bedroom, 2 bath rental home in Gilbert, Arizona can be currently (2018) purchased for about $250,000. To get the home in shape for renting may cost another $5,000 for a total investment of $255,000.

MOBILE HOME ON ITS OWN LAND

In our market a 3 bedroom, 2 bath mobile home on its own land can be purchased for around $90,000. A home purchased at this price will probably require about $10,000 in upgrades and repairs to get it ready for renting. A total of a $100,000 investment will be assumed.

MOBILE HOME IN PARK

Currently (2018) a 3 bedroom 2 bath home can be purchased for about $10,000. The home will require about $8,000 to get it into good rentable condition. The total investment in this scenario will be about $18,000.

In practice, park-based rentals trade lower upfront cost for higher control and regulatory risk, while land-based rentals trade higher acquisition cost for greater long-term stability.

|

| Traditional Site-Built Home | Mobile Home On Its Own Land | Mobile Home In A Park |

| Total Investment | $255,000 | $100,000 | $18,000 |

| Monthly Rental Value | $1,500 | $1,000 | $900 |

| Annual Rental Value | $18,000 | $12,000 | $10,800 |

| Park Rent Paid at $600 per month |

|

| ($7,200) |

| Taxes | ($1,500) | ($850) | ($175) |

| Annual Insurance | ($750) | ($750) | ($400) |

| Cash on Cash Annual Return | $18,000 – ($1,500) – ($750) = $15,750. — $15,750 / $255,000 = 6.18% ROI | $12,000 – ($850) – ($750) = $10,400. — $10,400 / $100,000 = 10.4% ROI | $10,800 – ($7,200) – ($175) – ($400) = $3,025. — $3,025 / $18,000 = 16.8% ROI |

| Annual Appreciation | 3% — $255,000 * 3% = $7,650 | 2.5% — $100,000 * 2.5% = $2,500 | 1.5% — $18,000 * 1.5% = $270 |

| Total Return (ROI) — Annual cash return plus annual appreciation | $15,750 + $7,650 = $23,400. $23,400 / $255,000 = 9.18% Total Annual ROI | $10,400 + $2,500 = $12,900. $12,900 / $100,000 = 12.9% Total Annual ROI | $3,025 = $270 = $3,295. $3,295 / $18,000 = 18.31% Total Annual ROI |

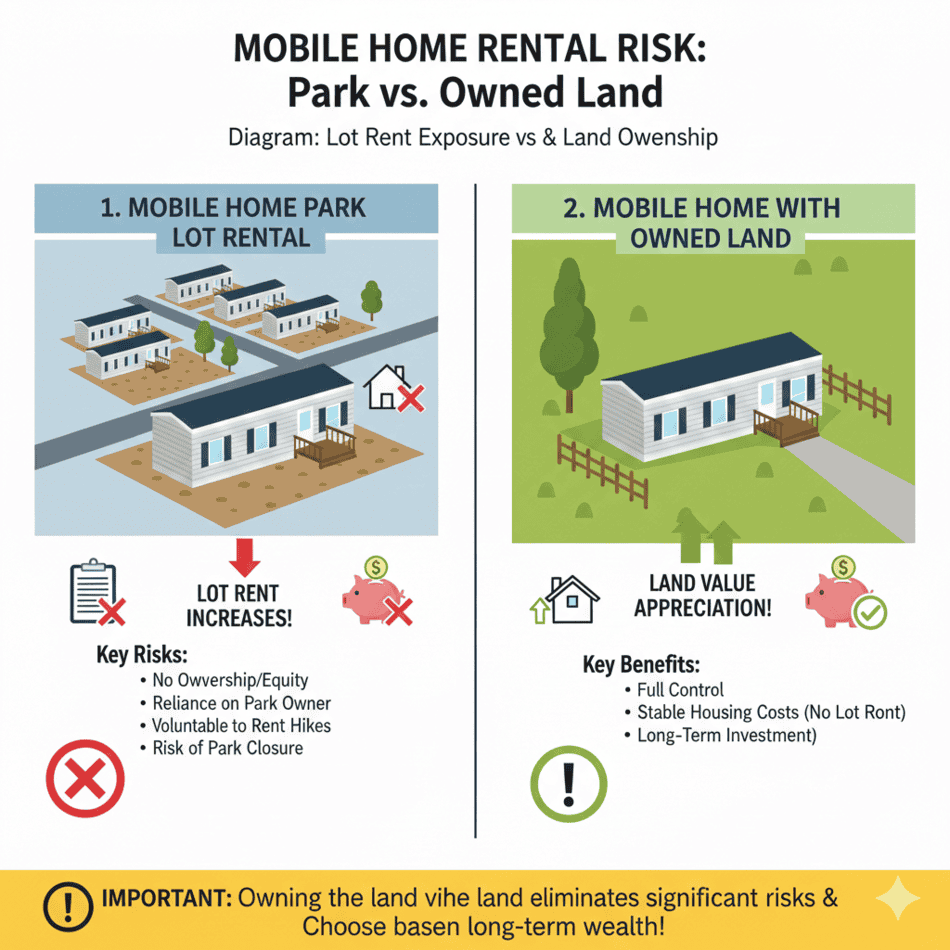

Mobile Home Rentals in Parks vs. On Owned Land

| Factor | Home in a Park | Home on Owned Land |

|---|---|---|

| Land Control | No control over land; subject to park ownership decisions | Full control of land and improvements |

| Lot Rent | Ongoing monthly expense; subject to increases | No lot rent; property taxes apply instead |

| Tenant Approval | Often requires park management approval | No third-party approval required |

| Eviction Process | Must comply with both landlord-tenant law and park rules | Standard landlord-tenant eviction laws apply |

| Financing Availability | Limited; typically personal property or chattel loans | Broader options if home is converted to real property |

| Insurance Availability | Can be restricted based on home age and park requirements | Generally easier to insure, especially with newer homes |

| Resale Liquidity | Dependent on park acceptance and buyer pool | Broader resale market, especially with land included |

| Appreciation Potential | Typically limited; depreciation is common | Land may appreciate even if the home depreciates |

| Regulatory Risk | Exposure to park rule changes and ownership transfers | Primarily subject to local zoning and housing codes |

| Exit Strategy Risk | Higher risk if park closes, changes rules, or denies buyers | Lower risk; land ownership provides flexibility |

As can be seen from the table above, mobile homes can offer an overall better total rate of return than a site built home. To realize good returns, for either a site-built home or a mobile home, the purchase has to be made correctly. If an investor overpays for any of the properties, the overall rates of return will be far lower.

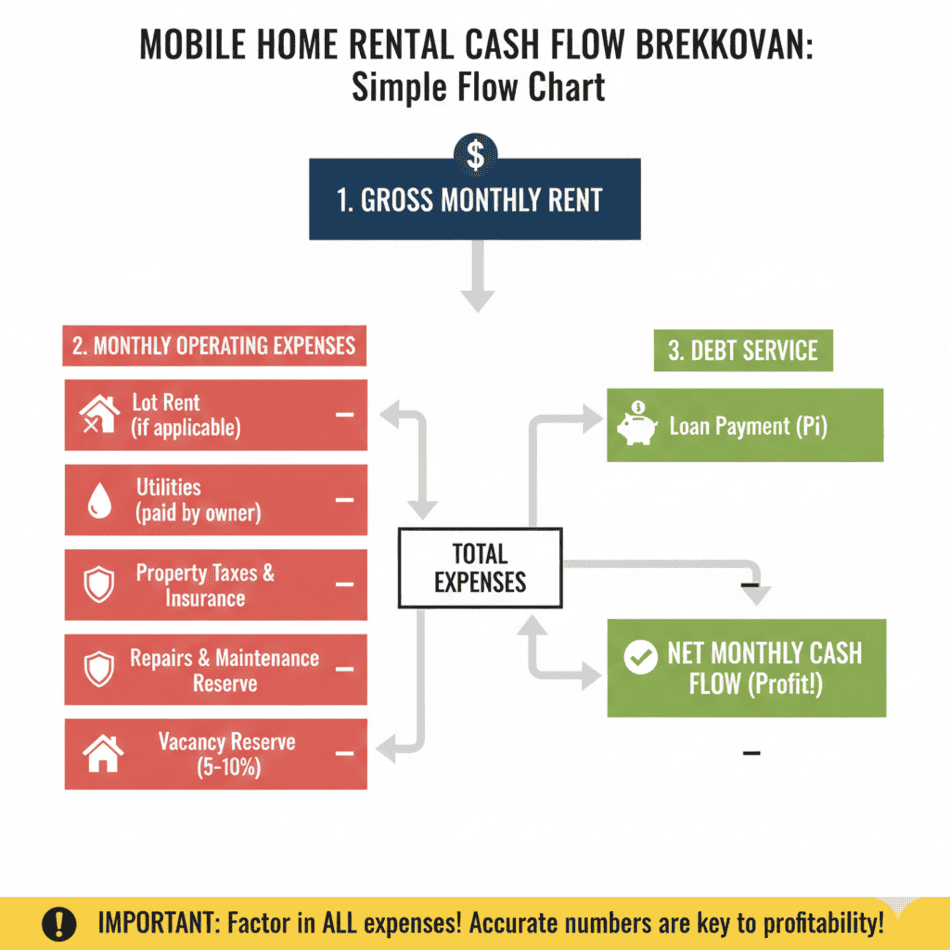

Illustrative Cost Structure Example (Not a Projection)

| Expense Category | Home in a Park (Example) | Home on Owned Land (Example) |

|---|---|---|

| Monthly Rent Collected | $1,100 | $1,300 |

| Lot Rent | $650 | $0 |

| Property Taxes | Minimal or included | $150 |

| Insurance | $90 | $120 |

| Maintenance Reserve | $100 | $100 |

| Estimated Net Before Vacancy | $160 | $830 |

These figures are illustrative only and do not represent typical or expected results. Actual outcomes vary based on location, home condition, financing, insurance availability, and regulatory factors.

Summary: Mobile home rentals in parks typically involve lower purchase prices but higher long-term control and regulatory risk, while rentals on owned land involve higher upfront costs but offer greater stability, insurance availability, and exit flexibility.

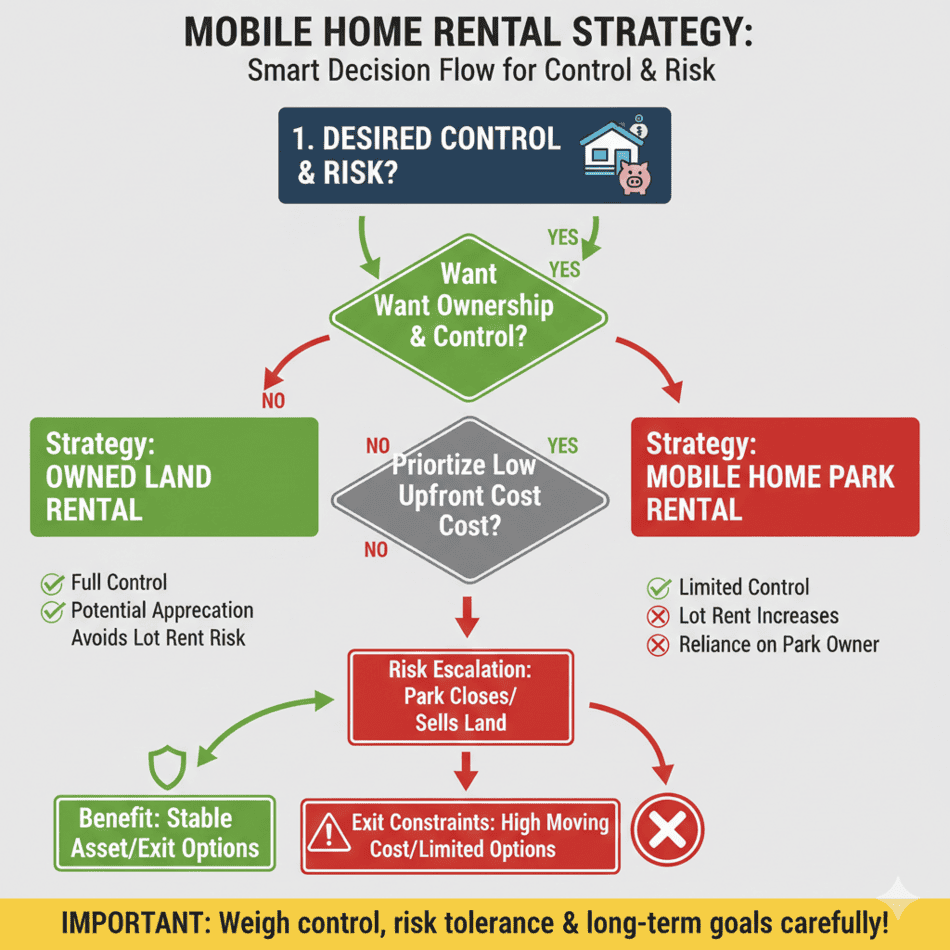

Park vs. Land Rental Decision Framework

- Does the investor control the land under the home?

- If no, proceed assuming exposure to lot rent increases and park rule changes.

- If yes, proceed assuming higher upfront cost but greater control.

- Is the home titled as personal property or real property?

- Can the home be insured at a reasonable cost?

- Does a third party control tenant approval or resale eligibility?

- Is the exit strategy dependent on park management cooperation?

If multiple answers depend on third-party approval, park-based rental risk is materially higher.

If you’re looking to invest in these types of real estate. Get to know your market well. Do your research, find out what the types of traditional homes or mobile homes in your area can be purchased for. As an investment, it is generally better to purchase a property that needs some TLC. It is far less expensive to do these repairs after you purchase the property, than to pay a house flipper for doing them for you before the purchase.

Whether the home sits in a park or on owned land fundamentally changes the investment profile. Lot rent exposure, park rules, and tenant approval processes can introduce risks not present on owned land. Investors evaluating park-based rentals should also review key considerations when buying a manufactured home in a park.

For additional context on how park ownership affects long-term outcomes, see this detailed discussion on buying manufactured homes in parks.

Mobile Homes Are Inexpensive To Renovate

Having renovated and flipped over 100 traditional homes, we’ve become pretty efficient at renovating on a tight budget to a standard that buyers expect. We have also renovated and flipped over 20 mobile homes. We have found in general that:

- Expectations – Buyers and renters of traditional site-built homes tend to have higher expectations than buyers and renters of mobile home properties.

- Roofing – Mobile homes have many different kinds of roofs. But, most of them are a simple rectangle. We have found that if a mobile home needs a new roof, it will generally cost less than have of what we spend on a reroof of a traditional home. On a mobile home we might spend around $1,000 to $3,000 on a reroof. For a traditional home that is usually $6,000 to $8,500.

- Flooring – In a mobile home we will usually use a combination of vinyl flooring and carpeting. In a traditional home we generally will do tile throughout. Our flooring renovation for a mobile home usually runs around $3,000 while the traditional home runs typically $5,500 to $9,000.

- Windows – Window replacement for a mobile home is usually less than half the cost of a traditional home. This is because mobile home windows generally come in a few standard sizes. They are also very easily removed and replaced. Mobile home window replacement generally costs us around $2,500 while traditional homes are about $4,500 to $8,000.

- Kitchens – We are generally able to install a lower grade of cabinet into our mobile home renovations. Also, mobile home kitchens tend to be smaller. Countertops are generally laminate in mobile homes where we do granite or quartz in site-built homes. We may spend $3,000 fully renovating a mobile home kitchen, where a site-built kitchen starts at about $6,000 and moves up from there.

- Bathrooms – Bathroom renovations also are far simpler in a mobile home. Access to plumbing is very easy. Also, shower and tub enclosures tend to be molded fiberglass. Replacing the cabinets, sink, toilet and tub/shower in a mobile home will usually cost around $1,500. That cost is about triple for a traditional home.

- Painting – This is where mobile homes can be more expensive that site-built homes. This is because many mobile homes have paneling or drywall covered in vinyl. Also, the wall panels in mobile homes are surrounded by several moldings, both vertical and horizontal. These usually have to be primed with Kilz type of primer. Also, all of the moldings need to be caulked to get a professional looking job. For a single-wide mobile home of about 900sf, we will usually spend about $3,000 for a full repaint inside and out.

Our experience has been that it takes about half the time for a mobile home renovation than for a traditional home. The benefits for an investor are many. Quicker turn-around, less expensive, and the buyer or renter has lower expectations. This is a win win situation.

Mobile Homes Are Inexpensive To Maintain

As an investor of both traditional single-family site-built homes as well as an investor of mobile homes, we find the mobile homes far easier to maintain.

Mobile homes are generally smaller, running about 800 to 1,400sf. Site-built homes are usually about 1,300 to 1,700sf for rentals. Systems in a mobile home are usually easier to access because of the crawl space underneath the home.

Plumbing and HVAC fixes are usually far less expensive. Also, regarding the HVAC system, we usually invest in used refurbished systems for the mobile homes when replacement is needed.

As an investor, we’re always looking for good handyman type of labor. We have one guy that has worked with us for years on our rentals and renovations. We are very familiar with what his capabilities are; and they are many. He is fast and charges us a rate of $20 per hour. Having good contractors that you trust and have worked with many times can be a life saver when it comes to investment properties.

Mobile Homes Have A Large Market Interested In Renting Them

In our real estate business, we often work with investors who are afraid of investing in mobile homes; even with the higher rates of return that mobile homes offer. When I ask them why, they usually admit to being fearful of the quality of tenant that they feel mobile homes will attract.

I started buying investment properties in the 1980s. Through the years I have owned many properties across different price ranges. This is what I have discovered over the years:

Buying Site-Built Homes Above The Median Price For The Area

- Rents are higher than typical rental rates

- Tenants usually want shorter term leases

- Tenant turnovers are extremely hard on a property and always cost plenty in additional renovations and lost rents

- Tenants tend to have very high expectations and call for the slightest of problems

- Not always, but often have excuses for late rental payments

Buying Site-Built Homes Below The Median Price For The Area

- Tend to rent fairly quickly

- Generally lower income tenants

- Tenants often have credit issues

- Tenants often pay late, but do pay the late fees which raises the overall rent received

- Tenants usually stay in the property for longer periods

- Tenants still tend to have high expectations and call for very small things

Buying Mobile Home Rental Properties

- Rent very quickly

- Generally low income tenants

- Tenants usually have lower credit scores

- Tenants often stay in the property for years as their other options are limited

- Tenants usually on-time with rent; many of mine pay early

- Tenant expectations are lower

- Tenants often fix small items on their own

- Park rental tenants are often harder to deal with and stay for much shorter periods

Mobile Home Tenants Tend To Stay Longer Than In Traditional Homes

Of all my rental experiences, I would say that mobile homes on their own land tend to be my favorite type of investment property. There are many renters looking for this type of property. The standards of a mobile home subdivision are usually lower than for a traditional neighborhood.

As most traditional neighborhoods now have homeowner associations, homes must be kept to a higher standard than most renters want to take care of. These tenants often have older cars and often work on them at the property. They are unable to do this in a traditional neighborhood. They often have older RV’s or trailers that they like to have on the property.

I usually find this not a problem. These tenants usually stay for many years. As long as they pay their rent on time and take care of the property I want to give them incentive to stay in the property. These tenants often have limited options when it comes to finding a property that will fit with their needs and lifestyle, keeping them in the property for much longer than usual.

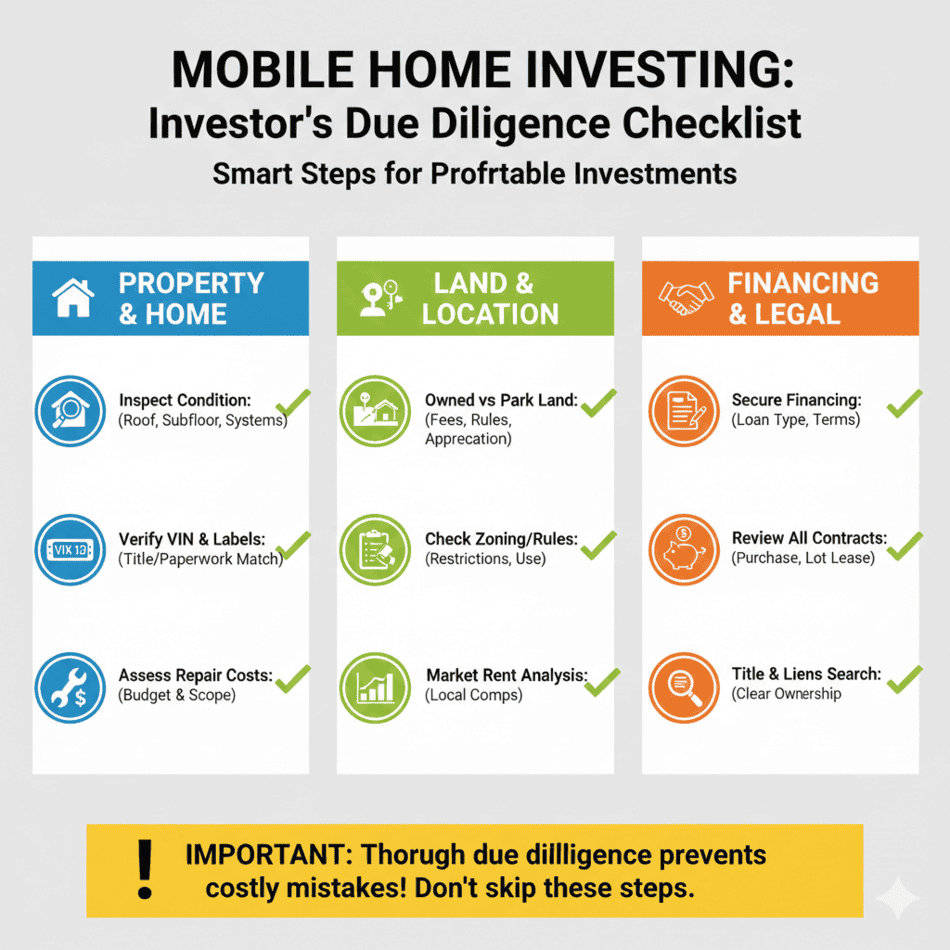

Mobile Home Rental Investment Due Diligence Checklist

- Confirm the home’s title status (personal vs. real property)

- Verify year of manufacture and HUD compliance label

- Confirm insurance availability and premium costs

- Review park rules, tenant approval process, and lot rent history

- Understand state eviction laws specific to manufactured housing

- Inspect structural, plumbing, electrical, and subfloor systems

- Assess resale liquidity and exit options before purchase

Physical condition plays an outsized role in rental performance for older manufactured homes. Deferred maintenance, subfloor damage, or improper setup can quickly erode cash flow. Investors unfamiliar with these risks should review why a manufactured home inspection is especially important before committing to a rental strategy.

Helpful Tool Suggestions

A basic moisture meter can help identify subfloor or wall moisture issues before they become structural problems. View a typical pin-type moisture meter on Amazon.

Older manufactured homes often have wiring issues that are not visually obvious. A simple outlet tester can reveal grounding and polarity problems. See an example outlet tester on Amazon.

Accurate interior measurements are useful when planning renovations or verifying advertised square footage. A basic laser distance measure can be found here.

Related Questions

1) HOW DOES RENTING A MOBILE HOME WORK?

There are really two types of mobile home rental investments as mentioned in the post above. The first is a mobile home in a park. The second is a mobile home on its own land.

Mobile Home In A Park – There are some parks that require the mobile home be “owner occupied”. This precludes renting them out. Other parks allow them to be rented. For those parks that do not allow “rentals”, an investor can usually sale the mobile home on “installments”. This is a whole other topic, but it has very good returns associated with it.

Most renters who rent a mobile home in a park are looking for the least expensive way to rent some housing. They tend to be far more “price sensitive” to the monthly rent amount than if the home was being sold on installments. Renters of a park mobile home also tend to be more nomadic and do not usually stay in the park long-term.

If you decide to rent out a mobil home in a park, you will collect the entire rent from your tenant – let’s say $850 per month – and then you must remit the park rent to the park management; park rent may be about $600 per month.

Mobile Home On Its Own land – As discussed in the post, this is my favorite type of mobile home investment. This rental would work the same as any other site-built home rental. You collect the rent, pay the insurance and property taxes and take care of any repairs. The great thing about this type of rental is that the tenants tend to stay for long periods, and the maintenance costs are usually far below a traditional rental home.

2) How Do I Make Money With Mobile Homes?

Fix and Flip – This is very popular right now for any property. Mobile homes can be especially profitable, but you have to make sure you purchase the home for the right price. We have found it possible to:

- Have homes owned by a mobile home park actually given to us for free or sold to us for very little

- Have received free lot rent during our renovation period

- Have had mobile homes in parks given to us by the owners or sold to us for as little as $1,000.

- Purchased mobile homes on their own land for as little as 1/3 of their renovated values

Keep in mind that these homes tend to be dilapidated and in very poor condition. We pretty much have to go through and / or replace every system in the home. But, we still find that if we are careful, the returns justify the risk.

Fix and Sale On Installments – This works pretty much the same as above. The only difference is that you are selling the home to the buyer for a down payment and then a note to be paid by the buyer over 5 to 8 years. Also, the note bears interest. We have sold many of these if we are not able to find a cash buyer in a reasonable amount of time.

A word of caution on this type of sale – you can quickly tie up your working capital in the notes receivable from your tenant buyers. Try to get enough down payment that your total investment in the home will be paid back within a year between the down payment and the payments received on your note.

About the Author: Charles O’Dell has over 25 years of experience in residential remodeling, property evaluation, and manufactured housing transactions. His work focuses on practical consumer education, investor risk analysis, and real-world outcomes rather than sales-driven assumptions.