Table of Contents

Introduction

Updated for 2025+: This article reflects current manufactured housing park conditions, including rising lot rents, ownership consolidation by regional and national operators, updated financing constraints, and recent state-level regulatory differences. The guidance below is intended for long-term buyers, retirees, and investors evaluating manufactured homes located in land-lease communities.

Manufactured homes can be found on either a piece of land that you own (fee simple) or on a rented lot in a mobile home park. If your aim is to buy a manufactured home, which option should you choose?

Video Guide Overview

Affiliate Disclosure: Some links on this page may be affiliate links. If you purchase through these links, MobileHomeFriend may earn a small commission at no additional cost to you.

The Short Answer

Short Answer: Buying a manufactured home in a park can make sense if lot rent stability, park ownership, lease terms, and exit options are carefully evaluated. The home itself may be affordable, but long-term costs and resale flexibility depend heavily on park rules, management practices, and state-specific protections.

- Why are you interested in living in a mobile home park?

- Manufactured homes in parks are considered personal property; not real estate.

- Park appearance can affect the value of the home either up or down.

- Monthly park rental prices will fluctuate over time.

- Monthly park rent is money you cannot recover.

- Mobile home park sets the standards for the neighborhood, much like an HOA.

Why Are You Interested In Living In A Mobile Home Park?

Before moving into a park, it is wise to ask yourself this question. The answer will likely be different for every resident, but knowing “your” reasons is an important step in making the decision. The reasons below are many that we have come across when selling mobile homes to buyers:

- The desire to own your own dwelling, where you can do what you like with your space. This means painting, walls, floors, kitchens, bathrooms, exterior, and the like. Owning the house itself allows you to make changes the way you would like without having to be concerned with a landlord.

- Not able to afford or qualify to purchase a stick-built house, townhouse, or condominium. This happens often. A buyer wants to get into the arena of home ownership, but cannot currently qualify to buy anything else. Purchasing a manufactured home in a park often allows a buyer the first step on the ladder towards ownership.

- Affordability – You may have enough money to pay for the manufactured home, but not enough income to qualify for a mortgage. In a park, there are homes in disrepair that can be purchased for little money. These homes can be renovated and value added when it is time to sell. This is often a way to make money when selling a manufactured home you purchase in a park.

- Not sharing walls. Many buyers have told us they resist living in an apartment or other dwelling where there are common walls. A manufactured home does not share any walls with a neighbor, giving the owner a stronger feeling of space and independence from others.

Whatever your reason, knowing why you are choosing a manufactured home in a park will help you decide on how much house, and at what price-point you’re willing to buy in a park, or lot that you do not own.

One commonly overlooked advantage is lower upfront land acquisition cost, which can reduce initial capital exposure compared to fee-simple property ownership. In many established parks, infrastructure such as roads, utilities, and community amenities are already maintained by the park owner, reducing owner responsibility.

However, buyers should confirm whether amenities advertised by the park are actively maintained or are legacy features no longer funded. Amenity quality can vary widely between owner-operated parks and those owned by large investment groups.

Manufactured Homes In Parks Are Considered Personal Property (Not Real Estate)

Currently we have a mobile home in a park listed for sale for a client. The home, a 1987 model, is in good, renovated condition. Being a 3 bedroom, 2 bath, doublewide in a good family park, it is getting 2 to 3 showings a day. It has been for the 3 weeks it has been listed.

Not surprisingly, most people have loved the home and many have wanted to buy it. What most of them don’t understand, including their agents, is that the home is not eligible for FHA, VA or other conventional financing. You see, a manufactured home on a leased lot, such as in a park, is not considered real estate. Instead, it is considered personal property, just like an automobile.

What this means is that the home is not eligible for financing as a piece of real estate. However, it may be financed as personal property. There are several companies out there that make loans on these types of homes. Keep in mind, that the payback term of the loan will likely be shorter that if it was real estate. Also, the interest rate will likely be higher as well.

Please visit the following sites that offer financing for manufactured homes in parks:

- https://www.multifamily.loans/mobile-home-park-financing

- https://www.scotsmanguide.com/pages/niche-lenders/mobile-manufactured-home-park-loans

- https://www.mobilehomeloans.com/loan-options/mobile-home-in-park-lending-2/

Park Appearance Can Affect The Value Of The Home Either Up Or Down

Certainly, all parks are not created equal. Some are impeccably maintained, while others can even look scary to drive through. So how does this affect the value of your manufactured home?

Parks, like any subdivision of homes, can be perceived as a desirable place to live, or it can be viewed as undesirable, or even dangerous. How that park is perceived will certainly affect the value of the manufactured homes in that park.

In our mobile home flipping, we have done homes in nicer parks, as well as some that are not so nice. What we found is that when we were in a park that might be a 3 or higher on a scale of 5, those homes would sell extremely quickly, even creating competition among potential buyers.

Parks that would be considered a 1 or 2 were much harder to get a good price for the home we were trying to sell.

One park in particular where we had done about 10 homes started going downhill. The management companies were turning over constantly. We finally had to stop doing any work in that park, because it no longer brought in the type of home buyer that would pay the prices we needed to make a profit on the homes.

You may find a home that appears to be a bargain in price when compared to other homes around town. But remember, that if you are going to live in that park, and if you plan on selling the home again at some point in the future, a run-down park may not be the best financial choice, even if it is less expensive.

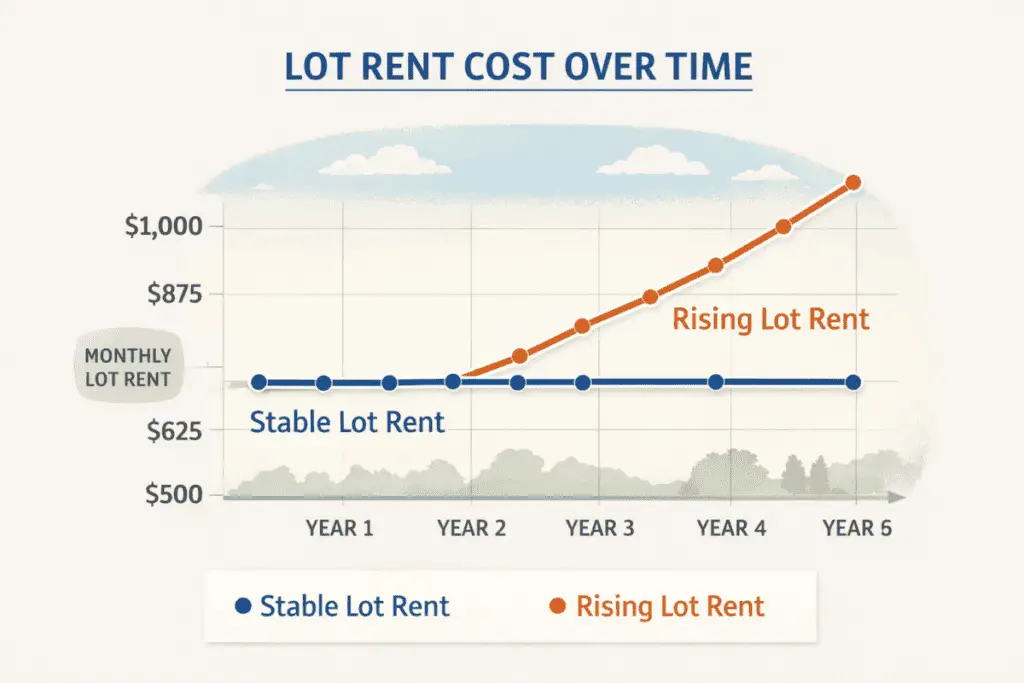

Monthly Park Rental Prices Will Fluctuate Over Time

In our area, Maricopa County, Arizona, base monthly lot rent prices for a family park can run from about $525 on the low side up to about $850 on the high side.

In addition to the base lot rent, you can also expect to pay for sales tax as well as utilities, (water, sewer). Trash is often included in the base lot rent price. These costs will add about an additional $50 to $75 per month over the base cost. Of course, prices will vary greatly around the country, so calling around your area of interest can give you a much better answer as to the monthly lot rent cost.

One thing is for certain, over the long haul, prices rise. Follow the link to a calculator that will let you pick an annual inflation rate, and see how your lot rent might increase over time.

The primary risk is lot rent volatility. Unlike fixed-rate mortgages, lot rent is typically subject to annual increases. While some states impose caps or notice requirements, others allow unrestricted adjustments. Buyers should request written lot rent history for at least the past five years.

Another common misunderstanding is assuming park rules are static. Park owners can revise rules governing pets, rentals, age restrictions, and home appearance, which may affect resale value or lifestyle suitability.

Mobile Home Lot Rent Cost Forecaster

Financing a Manufactured Home In A Park

Homes located in parks are often classified as personal property rather than real property, limiting access to traditional mortgage products. Chattel loans typically carry higher interest rates, shorter terms, and fewer consumer protections.

Buyers should verify whether the home is titled as real property or personal property and confirm lender acceptance before entering a purchase agreement. Financing availability can vary significantly by state and by park ownership policies.

Resale Value Influenced By Park

Resale value is influenced not only by the condition of the home but also by park reputation, management practices, and buyer eligibility rules. Some parks require prospective buyers to meet income thresholds or obtain park approval before a sale can close.

In higher-demand regions, well-managed parks can support stable resale values. In weaker markets, homes may become difficult to sell if lot rent increases outpace local housing alternatives.

Monthly Park Rent Is Money You Cannot Recover

By definition, rent is a payment made periodically by a tenant to a landlord in return for the use of rented object. In this case, that object is the lot on which your manufactured home sits in the park. You are only renting the lot, you do not own it.

If you are paying $700 per month overall in your lot rent, that is $8,400 per year. You did get the use of that land during the year, but your rent payment does not go towards building you any type of equity in the lot.

What price of land would your lot rent buy you?

Let’s make an assumption that you would rather own the land under your manufactured home, rather than live in a park. If you are paying $700 per month in lot rent, what price of lot could you afford if you were taking out a 20 year loan at 4% interest to make the purchase?

With these parameters, you could afford to purchase a lot valued at $115,000. If you are making the $700 per month payment toward your own lot, then you are building equity each month you make the payment, as well as the appreciating value of the lot.

Visit the following website to play around with different payment terms:

Internal Links To Helpful Articles

Before committing, buyers should understand how park ownership affects rules and costs. This is discussed in more detail in how to choose the right mobile home park, which explains ownership structures, rule enforcement, and warning signs.

Lot rent is a major long-term cost driver. For a breakdown of what lot rent typically includes and excludes, see what mobile home lot rent really covers.

Buyers comparing park homes versus land-owned options may also find value in the manufactured home buying process, which outlines title status, inspections, and closing considerations.

Optional tool: A compact high-lumen flashlight can help buyers inspect skirting, underfloor utilities, and crawl areas during walkthroughs. View flashlight on Amazon.

Manufactured Home Park Due Diligence Checklist

- Request written lot rent history (5+ years)

- Confirm park ownership and management company

- Review park rules, lease terms, and amendment rights

- Verify resale approval requirements

- Confirm utility responsibility and billing method

- Check state-specific tenant protections

- Verify home title status (real vs personal property)

Summary

A lot of people assume mobile homes are always found in mobile home parks; for example, the National Association of Manufacturers’ Mobile Home Way says 1.3 million people live in them which makes up about 5.7% of all housing units. But it is possible to buy a mobile home on its own land, which could be anywhere, even a large plot of

While it can be difficult for many to own a stick-built home, manufactured homes offer the chance to finally call a home your own. Buying a new one offers more customizability than ever before– whether you choose one that comes fully equipped or is in need of renovation. Mobile home parks are also an option if you don’t mind being surrounded by others. They may even have utilities and other benefits already in place.

The long-term cheaper option is to purchase your own parcel and put your home on your own property. This way you will avoid paying site fees that are lost forever as rent. About those site fees: buying in a mobile home park may be cheaper than buying land, but it still comes with costs. Most mobile home parks charge lot rent, which can vary widely depending on your location. That lot rent usually covers the costs of garbage pickup and grounds maintenance. Many parks charge you extra for water and sewage. (Home maintenance is up to you.) This happens in cases where you don’t own the land below your mobile home, just the house itself.

But in some parks, you may own the land. Those communities typically have a homeowners association (HOA) run by park developers or the residents. The HOA establishes community rules, and dues often run in the $200-$300/month range. Often trash, water, sewage, and park maintenance are covered by your dues. You’ll also need to follow the rules of the HOA, which might limit which colors you can paint your house and where you can park, among other things.

This article is based on long-term analysis of manufactured housing transactions, park ownership structures, financing models, and buyer outcomes across multiple U.S. markets. Information reflects common industry practices and publicly documented regulatory frameworks as of 2025.